2025 Social Security Taxable Maximum: FICA and Payroll Taxes [UPDATED]

As a business owner and an employer, you’re required to stay up to date with changes introduced by the Social Security Administration (SSA).

In 2025, SSA has introduced several updates that impact payroll and paystub generation.

Below, we summarize these key updates and provide guidance on ensuring compliance.

Read: What is OASDI?

Key Social Security Tax Changes in 2025

SSA has announced a few critical changes that employers should consider when generating paystubs:

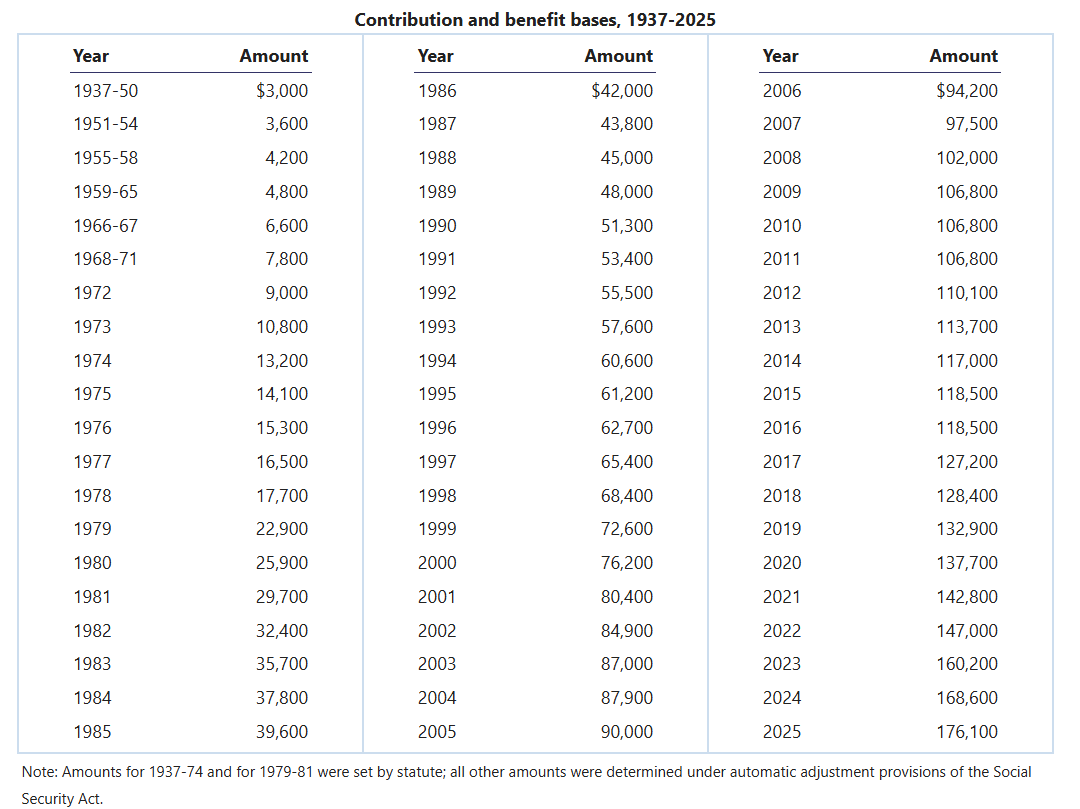

- The Social Security taxable maximum for 2025 has increased to $176,100, up by $7,500 from 2024. This means wages earned beyond this amount are not subject to Social Security tax.

- The Medicare tax remains unchanged and applies to all wages, with no income limit. Both employers and employees contribute 1.45% of wages, and high earners may owe an additional 0.9% Medicare tax.

Social Security and Medicare Taxes: What You Need to Know

The Social Security tax is one of the payroll taxes under the Federal Insurance Contributions Act (FICA) and funds retirement, disability, and survivor benefits. The FICA tax consists of:

- Social Security Tax (OASDI): 12.4% total (6.2% paid by the employer, 6.2% by the employee), applied only to wages up to $176,100 in 2025.

- Medicare Tax: 2.9% total (1.45% each from employer and employee), applied to all wages, with no cap.

- Additional Medicare Tax: Employees earning over $200,000 (single filers) or $250,000 (married filing jointly) must pay an extra 0.9%, but employers do not match this tax.

For 2025, the maximum Social Security tax an employee pays is $10,918.20, with employers contributing an equal amount. Self-employed individuals cover the full 12.4% on their own, meaning their maximum Social Security tax is $21,836.40.

SSA has provided a comprehensive FICA overview you can check out to familiarize yourself with the key numbers and percentages.

You may be interested: What is SUTA? Tax Rates, Obligations, Calculations

Managing Payroll with the 2025 Social Security Taxable Maximum

Employers must ensure their payroll systems reflect the updated Social Security taxable maximum of $176,100. This is crucial for accurate tax withholding and paystub generation. Since Medicare tax has no wage cap, all wages remain subject to at least 1.45% Medicare tax.

Given this new FICA limit, the maximum amount an employee and an employer will have to pay is 10,918.20 dollars each. For self-employed individuals, the amount is 21.836 dollars because they cover 12.4 percent of 176,100 dollars on their own.

As already mentioned, the Medicare tax isn’t subjected to a wage limit. The rate of 1.45 percent per employer and employee will have to be calculated, no matter how small or big the individual payment is.

Keep in mind, however, that employees who earn high wages may be subjected to an additional Medicare tax of 0.9 percent. This additional tax affects solely the employee and it doesn’t impact the amounts that employers have to pay.

The additional high income Medicare tax applies in various circumstances. These include:

-

Singe individuals who earn more than 200,000 dollars per year

-

Head of household (with qualifying person) who earns 200,000 dollars per year or more

-

Married couples filing jointly and earning more than 250,000 dollars

-

Married couples filing separately and earning wages of over 125,000 dollars

-

Qualified widowed individuals with a dependent child earning more than 200,000 dollars

The Cost of Living Adjustment (COLA) in 2025

COLA is an adjustment that’s made each year to the Social Security benefit amount. The Department of Labor is responsible for the creation of the annual Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) – the document upon which the COLA adjustment is based.

For 2025, the COLA has been announced at 2.5 percent. As per national statistics, 72.5 million people in the US will see an increase in their Social Security payments.

Additionally, employees who receive benefits before they reach the full retirement age (FRA) are always the subject of the retirement earnings test. This means that an income exceeding a certain amount will trigger benefits withholdings until the FRA is reached. This is another threshold that’s modified on an annual basis to reflect changes in economy and national finances.

There are two earnings test exempt amounts. The one is applicable to individuals who are younger than the retirement age and the other amount applies to those who are reaching the FRA over the course of the respective fiscal year. In 2025, the first amount is 23,400 dollars and the second one is 62,160 dollars.

To put that in simple terms – a person that earns 23,400 dollars or less (alternatively – 62,160 dollars or less) per year in 2025 will be eligible to receive Social Security benefits.

Final Thoughts: Stay Compliant with Payroll Changes

Keeping up with Social Security tax adjustments ensures compliance and accurate payroll reporting. Using payroll software or paystub generation tools can help businesses adapt quickly to these annual changes.