FUTA Taxes: Definition, Calculations, How to Pay, and How to Report

FUTA taxes are a federal tax requirement employers must follow if specific criteria are met. FUTA taxes are used to help state and federal jobless compensation programs. The initiatives are designed to provide temporary financial help to workers who have lost their jobs.

FUTA taxes are calculated by determining a specified proportion of an employee's wages up to a specific wage base. The federal unemployment tax rate is now 6% of the first $7,000 of each employee's annual wages. Companies have an option to claim a credit of up to 5.4% for state unemployment taxes paid, essentially lowering the FUTA tax rate to 0.6% for the majority of companies.

Employers needed to settle FUTA taxes. The taxes are not kept from employee wages and are completely the employer's obligation. FUTA taxes are paid to the Internal Revenue Service (IRS) periodically. Employers use the Electronic Federal Tax Payment System (EFTPS) or involve the payment with the federal tax return to pay FUTA taxes.

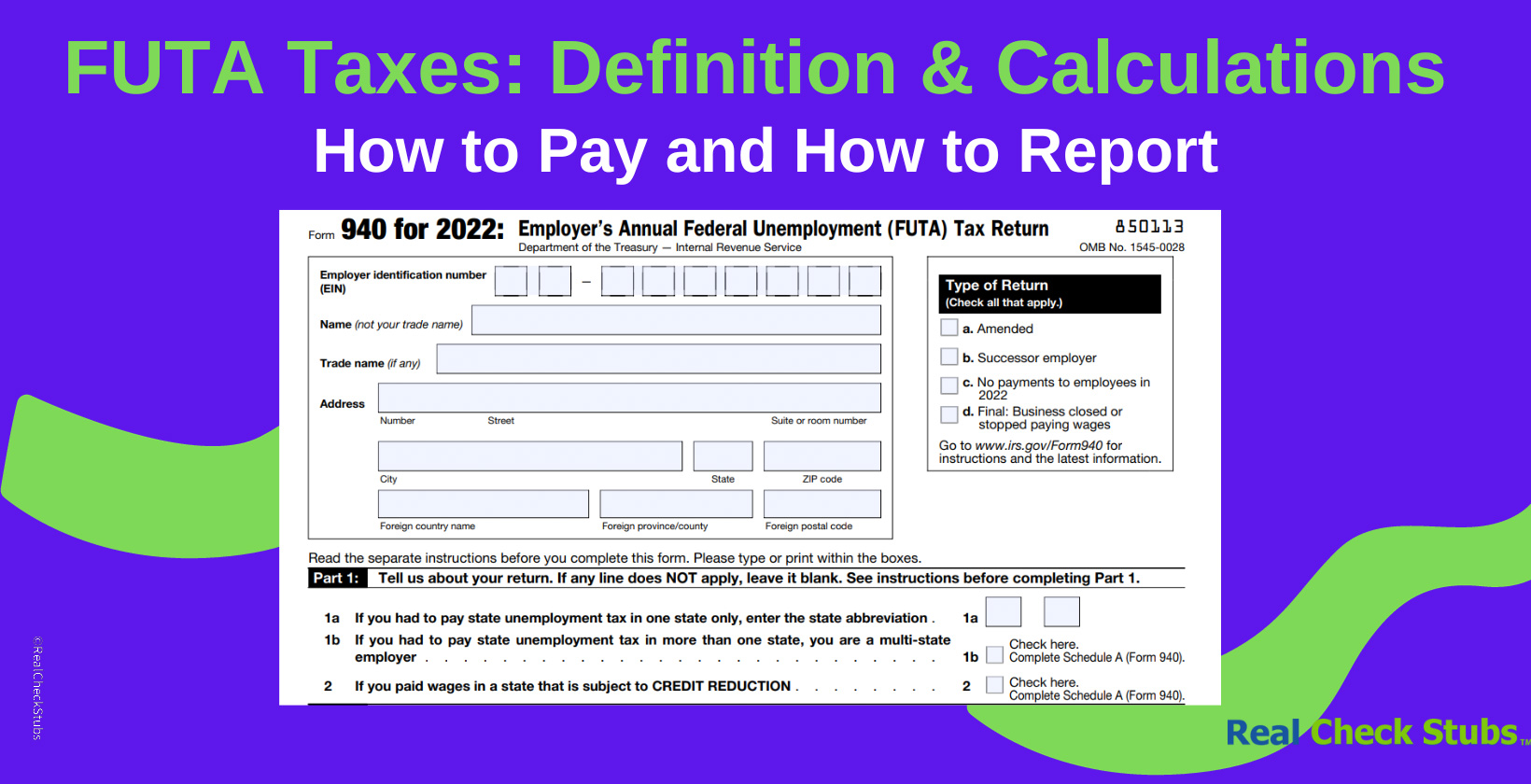

Reporting FUTA taxes involves completing an annual document known as document 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return. Employers use the form to determine and report their federal unemployment tax liability for the current year. The Form 940 filing deadline is January 31 of the following year. Employers that have punctually deposited all taxes have until February 10 to file the form.

What is FUTA Tax?

FUTA Tax is a federal tax charged to employers in the United States. Employers must make a mandated contribution on behalf of their workers to fund the federal unemployment insurance program. The program aims to provide temporary financial help to people who lose their jobs through no fault.

Employers must settle a portion of their employee's salary, up to a specific wage base, into the federal unemployment insurance system under the FUTA Tax. The present FUTA tax rate is 6% of the first $7,000 of each employee's annual salary. Companies claim a credit of up to 5.4% for paying state unemployment taxes, lowering the FUTA tax rate to 0.6% for most companies.

The revenues raised through FUTA taxes are used to manage federal unemployment benefits. The benefits provide short-term financial help to people actively looking for work after losing their jobs. The money helps to keep the unemployment insurance program running smoothly.

SUTA Tax is an abbreviation for State Unemployment Tax Act Tax. Individual states charge a similar form of tax to finance their separate state unemployment insurance systems. SUTA taxes are distinct from FUTA taxes and are managed state-by-state. SUTA tax rates and wage bases differ from state to state.

SUTA taxes are known by several names depending on the state or region. The names include State Unemployment Insurance (SUI) tax, State Unemployment Compensation (SUC) tax, and State Unemployment Tax (SUT) in general. The names are used interchangeably to refer to the tax paid by employers to fund state unemployment insurance systems.

What is the purpose of the FUTA Tax?

The purpose of the Federal Unemployment Tax Act (FUTA) Tax is to provide funding for the federal unemployment insurance program in the United States. The FUTA Tax ensures that funds are available to provide temporary financial support to workers who become unemployed due to circumstances beyond their control.

The Department of Labor's federal unemployment insurance program seeks to give qualified people a temporary earnings replacement while they search for new employment. The initiative reduces financial challenges caused by unemployment and promotes economic stability.

The FUTA Tax is one of the program's revenue sources. Employers must provide for the program by paying a portion of their employees' wages into the federal unemployment insurance system up to a certain wage base. The funds are then utilized to pay qualified workers' unemployment benefits.

FUTA Tax offers a safety net for workers facing temporary job loss by establishing a nationwide structure for unemployment insurance. The gathered tax income aids in the general administration of the unemployment insurance program, including benefit disbursements, job search assistance, and re-employment programs.

The FUTA Tax is intended to enhance labor market stability by decreasing the economic burden on people and families during periods of unemployment. FUTA Tax motivates people to actively seek new job opportunities and helps keep consumer spending levels stable, which benefits both local and national economies.

How important is FUTA Tax in Payroll?

FUTA Tax is very important in payroll for employers in the United States. FUTA Tax is not just a legal necessity, but it additionally serves a substantial role in supporting the federal unemployment insurance program and preserving economic stability.

Employers are needed by federal law to follow tax requirements, which include paying the FUTA Tax. Failure to meet the commitments results in sanctions and legal consequences. Employers must pay the utmost attention to the calculation and submission of FUTA Tax to ensure compliance and prevent any consequences.

Financing the federal unemployment insurance program is one of the principal goals of the FUTA Tax. Employers provide a safety net that gives brief financial help to workers who become unemployed through no fault of their own by paying the tax. Cash support lessens the impact of job loss and provides clients with stability while they look for new employment.

Having unemployment benefits available through the federal insurance program helps to balance the economy during economic downturns or localized job losses. Employers ensure that funds are available to provide unemployment benefits to qualified persons by contributing to the FUTA Tax. FUTA tax support keeps consumer expenditure levels stable, supporting businesses and general economic activity.

The FUTA Tax money goes toward the administration of the federal unemployment insurance program. The funds are used to assist in the administration of unemployment claims, the processing of benefit payments, the provision of job search support, and the provision of reemployment programs. Employers indirectly contribute to the proper operation of the program by providing the infrastructure required to administer unemployment benefits.

Tax compliance and reporting are FUTA processes. Employers must accurately report FUTA Tax responsibilities, file the required forms, and make timely payments to the Internal Revenue Service (IRS). The FUTA tax report promotes transparency, accountability, and conformity to tax requirements, preserving the payroll process's integrity.

How to Calculate FUTA Tax?

Listed below are steps on how to calculate FUTA Tax.

- First, perform the FUTA Taxable Wages calculation to determine each employee's FUTA Taxable Wages. Remember that the FUTA Tax applies to the first $7,000 in annual pay for each employee.

- Second, determine the FUTA Taxable amount. The FUTA Taxable Wages of all employees must be added together to determine the overall amount.

- Third, multiply the FUTA taxable amount by the 6% FUTA tax rate that is in effect at the time. It determines the FUTA Tax due before taking into account credits.

- Fourth, Check whether the state has a suitable unemployment tax program in place. Multiply the FUTA Taxable Amount by the state's unemployment tax credit rate, which is often up to 5.4%, to determine the credit.

- Fifth, reduce the FUTA Tax burden determined by the State Unemployment Tax Credit. The outcome indicates the total amount of FUTA Tax due.

- Sixth, check the Maximum Taxable FUTA Amount. Make sure that the net FUTA tax liability is no more than $420 (6% of $7,000), which is the most amount that is deducted from each employee's paycheck.

How is FUTA Tax liability computed for multi-location employers?

Multi-location employers must aggregate their employees' pay from each location to calculate their FUTA Tax due. The process requires totaling the FUTA Taxable salaries across all sites to calculate the total FUTA Taxable wages for the entire firm. Employers properly determine their entire tax liability if they consider earnings from all locations.

Calculating the FUTA Tax liability for multi-location firms entails aggregating wages and taking into account location-specific tax rates and credits. The FUTA Tax due must be determined separately for each location because the state unemployment tax rates vary depending on the location. It guarantees that the tax liability appropriately represents the wages and tax rates applicable to each given location.

Each location is subject to a different state unemployment tax rate. The fees differ based on the state in which each site is located. Determining and accounting for the applicable tax rates for each location is critical. Employers compute the FUTA Tax liability for each site more precisely by incorporating the correct tax rates.

Employers with many locations must consider state unemployment tax credits applicable to each location. The credits differ by state and have an impact on the total FUTA Tax payment. Calculating the state unemployment tax credit separately for each location ensures that the FUTA Tax liability appropriately reflects the available credits.

What is the current FUTA Tax Rate?

The 2023 FUTA Tax rate of 6% of the first $7,000 of each employee's yearly wages represents the continuation of the federal government's existing rate. Employers are required to contribute to the federal unemployment insurance program based on a percentage of their employees' wages at a 6% FUTA tax rate. The FUTA Tax is intended to support unemployment benefits granted to workers who are laid off involuntarily.

The 6% rate means that businesses must contribute 6% of the first $7,000 of each employee's wages per year to the FUTA Tax. The rate indicates that an employer's maximum FUTA Tax liability per employee is $420 ($7,000 x 0.06). Employers must calculate and remit the tax to the Internal Revenue Service (IRS) according to the specified schedule.

Employers must appropriately calculate and pay the FUTA Tax to meet their commitments and support the federal unemployment insurance program. The FUTA Tax is critical in providing temporary financial support to qualifying individuals who become unemployed due to no fault of their own. Employers contribute to a safety net that helps ease the financial costs of unemployment and supports individuals as they actively seek new employment possibilities by paying the FUTA Tax.

Employers must calculate and pay the FUTA Tax correctly to meet their obligations and support the federal unemployment insurance program. The FUTA Tax is crucial in providing temporary financial assistance to qualifying individuals who become unemployed due to circumstances beyond their control. Employers contribute to a safety net that helps lessen the financial expenses of unemployment and assists individuals while they actively seek new employment opportunities by paying the FUTA Tax.

Does the FUTA Tax Rate vary from different States?

No, the FUTA Tax rate does not vary from state to state. The FUTA Tax rate is a federal tax rate that is consistent throughout all states in the United States. The FUTA Tax rate is set at 6% of the first $7,000 of wages per annum for all employers nationwide.

States impose their own unemployment taxes, known as the State Unemployment Tax Act (SUTA), while the FUTA Tax rate is consistent. SUTA taxes are diverse from FUTA taxes and differ by state. Each state has its own SUTA tax rate, earnings basis, and employer restrictions.

Employers are liable for both FUTA Tax and state SUTA taxes, each with its own set of computations and reporting requirements. State-specific SUTA tax rates and rules differ, and employers must follow the laws of the states in which they operate.

Employers must refer to the specific rules and resources offered by each state's unemployment tax office to guarantee compliance with FUTA taxes and state SUTA taxes. The resources provide the most up-to-date and correct information on state-specific unemployment tax rates and requirements.

Is it possible to calculate FUTA tax using a Paystub Generator?

No, it is not feasible to calculate FUTA tax using a Paystub Generator. A Paystub generator does not include the exact calculations required for FUTA Tax, but it helps with generating paystubs and providing information on employee earnings, deductions, and withholdings.

Calculating FUTA Tax involves considering elements such as FUTA Taxable wages, FUTA Tax rate, state unemployment tax credits, and other applicable requirements. The computations require knowledge of the employee's wages and extra information not commonly supplied on a paystub.

Refer to the most recent IRS laws and recommendations, use authorized IRS forms, or use specialized payroll software or tax preparation software that includes FUTA Tax computations to calculate FUTA Tax accurately. The tools are specifically intended to manage the intricacies of FUTA Tax calculations, considering all relevant variables and ensuring accuracy.

A paystub generator provides useful information in calculating FUTA Tax, but it is insufficient to produce a complete and correct FUTA Tax computation. Relying on relevant tools and references built expressly for FUTA Tax calculations is critical to maintaining compliance with tax requirements. Employers must use comprehensive FUTA Tax computation tools to correctly determine their employees' FUTA tax responsibilities and meet tax laws, rather than relying on a paystub generator.

How to Report FUTA Tax?

Begin by filling out Form 940 which is designed exclusively for reporting FUTA Tax responsibilities and credits. Fill out the form with the required employer data, such as the employer identification number (EIN), legal name, address, and contact details.

Compute the FUTA Tax liability by accurately determining the FUTA Taxable wages. Calculating involves identifying the wages subject to FUTA Tax and applying the current FUTA Tax rate. Take into consideration any applicable state unemployment tax credits that help lessen the overall FUTA Tax liability.

Record it on Form 940 in the appropriate sections once the FUTA Tax Liability has been calculated. Be diligent and ensure that all information is accurate and complete to avoid any discrepancies.

Assess whether deposits or payments are needed for the reported FUTA Tax liability. Deposits are necessary if the accumulated FUTA Tax liability exceeds $500 during a calendar quarter. Familiarizing oneself with the IRS guidelines and deposit requirements helps determine the specific obligations.

Submit Form 940 to the Internal Revenue Service (IRS) by the deadline when everything is in order. The filing deadline for each tax year varies. Keep detailed records of the FUTA Tax reporting and payments, including copies of Form 940 and any supporting paperwork.

Do agricultural workers and household employees have specific FUTA tax rules?

Yes, agricultural workers and household employees have specific FUTA tax rules. The FUTA tax laws give agricultural workers particular exemptions and special advantages. Employers must pay the FUTA tax if they pay agricultural workers wages of $20,000 or more in a calendar quarter or if they hire 10 or more agricultural workers for at least a portion of each day for 20 weeks in a row. The employer is not obligated to pay FUTA tax on the wages paid to agricultural employees if neither of the thresholds is met.

Domestic employees are covered by the FUTA tax laws. Employers are required to pay FUTA tax if they pay cash wages of $1,000 or more to a household employee during any calendar quarter of the current or prior calendar year. Home workers are exempt from FUTA tax if their company pays them less than $1,000 in any calendar quarter.

Employers employing farm and home workers are required to comprehend and abide by the particular FUTA tax requirements. Employers must examine the IRS's guidelines and publications or seek professional advice to ensure compliance with the regulations and properly calculate their FUTA tax responsibilities for agricultural and home employees.

How to Pay for FUTA Tax?

Begin by evaluating the best payment schedule for the FUTA tax liability. Futa Tax is resolute by whether the liability surpasses $500 in any given quarter or if the overall liability for the year is less than $500, allowing for an annual payment.

Quarterly payments are necessary if the FUTA tax liability for a quarter exceeds $500. Determine the liability for each quarter by calculating the FUTA tax owed. Submit the payment by the due date, which is usually the last day of the month after the quarter's conclusion. Payments are required by April 30th for the first quarter, July 31st for the second quarter, October 31st for the third quarter, and January 31st for the fourth quarter. An annual payment option is available if the total FUTA tax burden for the year is less than $500. Calculate the overall liability for the year and make one payment by the due date.

Consider using automated payment methods such as the Electronic Federal Tax Payment System (EFTPS) for simplicity and efficiency. Enroll in EFTPS and plan ahead of time to ensure timely transactions. Additional options include sending a check or money order with the payment voucher by mail or using IRS Direct Pay.

File Form 940, the Employer's Annual Federal Unemployment (FUTA) Tax Return, regardless of the payment schedule chosen. The form reconciles payments and reports the overall FUTA tax liability for the fiscal year. Fill out the form completely and return it before the deadline. Maintain comprehensive records of FUTA Tax payments. Keep payment confirmations, copies of Form 940, and any supporting paperwork for the IRS-mandated period.

Who should pay FUTA Tax?

The employer must be paying for FUTA Tax, not the employee. The FUTA Tax, which stands for Federal Unemployment Tax Act, is a payroll tax levied on employers to finance federal unemployment benefits. It is an employer-side tax that is distinct from the income taxes taken from employees' wages.

Employers are responsible for calculating and paying FUTA Tax based on the wages paid to their employees. The tax is calculated at a rate of 6% on the first $7,000 of each employee's annual wages. Employers are eligible for a tax credit of up to 5.4% if they pay their state unemployment taxes promptly.

Employers must calculate and pay FUTA Tax based on the wages paid to their employees. The tax is determined at a rate of 6% on the first $7,000 in annual wages for each employee. Employers are entitled to a tax credit of up to 5.4% if they pay their state unemployment taxes on time.

What is an exception to the FUTA Tax?

An exception to the FUTA Tax is that certain types of nonprofit organizations are exempt from paying it. Governmental bodies, such as the federal, state, and municipal governments, are specifically excluded from the FUTA Tax. Government agencies, departments, and instrumentalities are included.

Governmental organizations are exempt from the FUTA Tax since they often have their own systems in place to benefit their employees. The systems are funded through alternative ways, such as government-specific levies or self-insurance plans. Governmental entities are subject to other employment taxes, such as FICA taxes and state unemployment taxes, depending on the relevant laws and regulations.

Certain types of nonprofit organizations, such as religious organizations and agricultural labor organizations, are exempt from the FUTA Tax. The requirements for exemption vary, and it is recommended that these organizations check the IRS guidelines or obtain expert guidance to ascertain their exact exemption status.

What is the consequence for late payment of FUTA taxes?

The consequence of the late payment of FUTA taxes is the potential imposition of penalties and interest charges by the Internal Revenue Service (IRS). The overdue amount is higher, with penalties and interest starting when the tax payment was initially due.

There is commonly a penalty of 2% of the total amount owed in taxes for each month or portion of a month that FUTA taxes are paid late. The penalty rises to a maximum of 25% if the payment is persistently late.

The IRS imposes interest on the unpaid tax amount in addition to penalties. The IRS sets the daily compounded interest rate. Interest is assessed from the first tax payment due date until the whole amount is paid.

Fulfill the FUTA tax payment obligations on time and accurately to avoid fines and interest charges. Employers must understand the specific payment deadlines, correctly estimate their tax obligations, and submit timely payments. Contact the IRS to discuss the options if quick payment is impossible, such as setting up monthly payments to pay off the back taxes.

Can FUTA taxes be paid electronically?

Yes, FUTA taxes are paid electronically. The Electronic Federal Tax Payment System (EFTPS) is the preferred way for paying FUTA taxes electronically. EFTPS is a secure online system provided by the United States Department of the Treasury that allows taxpayers to make federal tax payments, including FUTA taxes, electronically.

Employers must enroll in the system and create a payment profile before they use EFTPS. Payments are booked in advance once enrolled, assuring prompt and convenient transactions. EFTPS allows taxpayers to track their payment history and receive electronic confirmation of payments.

EFTPS and other electronic payment methods have various advantages, including accuracy, efficiency, and ease. Employers calculate their FUTA tax amounts, schedule payments, and get confirmation electronically, reducing errors and streamlining the payment process.

The IRS provides several electronic payment alternatives. Taxpayers use the IRS website to make payments directly from their bank accounts utilizing the IRS Direct Pay system. It is a free and secure electronic payment method.

Employers use authorized payment processors to make electronic FUTA tax payments. The processors charge fees for their services, which is why it is necessary to read the terms and conditions before employing third-party payment processors.

What are the Benefits of FUTA Tax?

Listed below are the benefits of FUTA Tax.

- Unemployment Insurance Coverage: The FUTA Tax supports the federal unemployment insurance program, which offers financial assistance to workers who are laid off through no fault of their own. The coverage assists individuals in meeting their basic necessities while looking for new job prospects.

- Stable Workforce: FUTA Tax helps to keep a stable workforce by giving unemployment compensation. Workers who are laid off have access to short-term financial support, which reduces the risk of financial hardship and promotes stability throughout periods of unemployment.

- Economic Stability: FUTA Tax-supported federal unemployment insurance helps to keep the economy stable when the economy is weak. FUTA Tax lessens the impact of job losses by giving economic support to individuals, allowing them to continue spending on necessities.

- Reduced Poverty and Social Impact: FUTA Tax helps prevent individuals and families from falling into poverty due to sudden job loss. Unemployment benefits provide a safety net and alleviate the financial strain faced by affected individuals and their households.

- Reemployment Support: FUTA Tax funds are used to support various reemployment initiatives and services. The resources assist unemployed individuals in finding new work prospects by providing job training, job search assistance, and other supportive services.

- State Partnership: The FUTA Tax is a federal tax that collaborates with state unemployment tax systems. FUTA Tax establishes a framework for federal and state agencies to work together to run unemployment insurance systems and distribute benefits effectively.

- Employer Assistance: Employers claim a tax credit for payments paid into state unemployment insurance funds under the FUTA Tax system. The benefit serves to offset a portion of the FUTA Tax liability and assist qualifying employers in decreasing their overall tax load.

- Social Safety Net: The FUTA Tax contributes to the social safety net by providing qualified persons with temporary financial help, assuring income stability during unemployment.

What are the Limitations of FUTA Tax?

Listed below are the limitations of FUTA Tax.

- Limited Coverage: The FUTA tax is relevant to businesses with at least one employee on-site for any part of a day during each of 20 or more weeks in a year. Specific types of employees, such as independent contractors and domestic workers, are exempt from the FUTA tax.

- Taxable Wage Base: The first $7,000 of each employee's pay earned during a calendar year is subject to the FUTA tax. An employee's eligibility for FUTA tax is no longer valid once their pay exceeds the threshold.

- State Unemployment Tax: Employers subtract any state unemployment taxes they pay from their FUTA tax obligation. The FUTA tax burden increases if a state's unemployment tax rate for employers is low or nonexistent.

- Yearly Variations: The FUTA tax rate alters yearly depending on how the federal government assesses the needs of the unemployment trust fund. It leads to unpredictability in employer tax planning.

- Administrative Burden: The administrative burden of calculating, withholding, reporting, and remitting FUTA tax is the employer's responsibility. Rules compliance is challenging for small businesses and large enterprises with intricate payroll systems.

- Limited Use of Funds: The federal unemployment trust fund is the main recipient of FUTA tax funds, which are then utilized to keep unemployment benefits in place. The money is not managed or utilized under the direct supervision of the employers.

- Not Based on Employer Unemployment Experience: FUTA tax rates are not determined by an employer's unemployment history. FUTA tax rates are the same for all covered businesses regardless of the number of layoffs a company has experienced.

- No Impact on State Unemployment Benefits: FUTA tax contributions have no immediate effect on the sum or duration of unemployment benefits received by eligible workers. State law regulates the provision of unemployment benefits.

How does FUTA Tax differ from other types of Payroll Taxes?

FUTA tax is designed to fund unemployment benefits for eligible workers, unlike Social Security and Medicare taxes, which are known as Federal Insurance Contributions Act (FICA) taxes. FICA taxes finance Social Security retirement and disability benefits, together with Medicare healthcare coverage for retirees.

FUTA and FICA taxes have very different taxable pay basis. The first $7,000 of an employee's pay is subject to Federal Unemployment Tax Act (FUTA) tax, regardless of their total annual earnings. The FICA tax base for Social Security and Medicare are separate. Earnings exceeding $160,200 are not subject to Social Security taxation, as the program sets a cap. All income is subject to Medicare tax, without any threshold at which wages become exempt.

The FUTA tax rate is often lower than the combined rate for Social Security and Medicare. The Federal Unemployment Tax Act (FUTA) imposes a 6% tax on taxable earnings. Most firms are eligible for a credit of up to 5.4% if they pay their state unemployment taxes on time. The FUTA tax rate is 0.6% low. Social Security and Medicare FICA taxes add up to 15.3 percent. Employers contribute 7.65 percent, while employees cover the remaining 8.35 percent.

Another noteworthy distinction is the distribution of cash. The majority of the money collected from FUTA taxes is allocated to assisting those who are unemployed. FICA taxes, which fall under the types of payroll taxes, are used to pay specific government benefit programs such as Social Security retirement and disability benefits.

How do FUTA Taxes differ from SUTA Taxes?

FUTA taxes and SUTA taxes differ in their scope, administration, and objective. The Federal Unemployment Tax Act, or FUTA, is a federal tax charged on employers to pay the federal unemployment trust fund. The revenues raised through FUTA taxes are accustomed to support workers who become unemployed and are eligible for unemployment benefits. The current FUTA tax rate is 6% on the first $7,000 in wages for each employee. Businesses claim a credit of up to 5.4% by paying their state unemployment taxes on time, lowering the FUTA tax to 0.6%.

SUTA, or State Unemployment Tax Act, refers to state-level unemployment taxes paid by businesses to fund state-provided unemployment benefits. There are differences across states since SUTA tax rates and wage bases are determined independently by each state. The SUTA tax rate depends on an employer's unemployment experience, which conveys that enterprises with a higher layoff history incur higher SUTA tax rates. The pay base for SUTA taxes varies by state, as opposed to the consistent $7,000 wage base for FUTA taxes.

The distribution of funds is a key distinction between FUTA and SUTA taxes. Federal FUTA taxes are remitted to states to finance their unemployment programs, but each state keeps separate accounts for administering its unemployment funds. FUTA contributions do not benefit specific employees in a given state. Employers are obligated to record and pay both FUTA and SUTA taxes, but they must do so separately. FUTA taxes are recorded on Form 940, while SUTA taxes are reported on state-specific forms required by each state's workforce agency.

How do FUTA Taxes differ from FICA Taxes?

FUTA taxes and FICA taxes are two distinct types of payroll taxes in the United States, each serving different objectives and funding specific government programs.

The Federal Unemployment Tax Act, or FUTA, is a federal tax charged on employers to fund the Federal Unemployment Trust Fund. The fundamental objective of FUTA taxes is to offer financial support to eligible workers who are laid off due to circumstances beyond their control. The FUTA tax revenue is allocated to state workforce agencies to assist in paying state unemployment benefit programs. The current FUTA tax rate is 6% on the first $7,000 in wages for each employee. Employers often claim a credit of up to 5.4% if they pay their state unemployment taxes promptly, essentially lowering the FUTA tax rate to 0.6%.

FICA taxes, or the Federal Insurance Contributions Act taxes, consist of two components which are the Social Security tax and the Medicare tax. Employers contribute to the taxes, which are taken from employees' wages. The Social Security tax pays for retirement and disability benefits for eligible persons, whereas the Medicare tax pays for retiree healthcare coverage. The overall FICA tax rate is 15.3%, with employees and employers each paying half (7.65%).

Another distinction between FUTA and FICA taxes is the taxable wage base. The taxable wage basis for FUTA taxes is $7,000 per employee per calendar year, regardless of total yearly income. Each component of FICA taxes has its wage base, which implies that employees must pay Social Security tax on income up to a particular threshold, whereas the Medicare tax has no wage base limit.

The revenues raised through FICA taxes are not used to finance unemployment benefits directly. They are instead used to fund certain government benefit programs, such as Social Security retirement and disability payouts, along with Medicare healthcare coverage for seniors.

Kristen Larson is a payroll specialist with over 10 years of experience in the field. She received her Bachelor's degree in Business Administration from the University of Minnesota. Kristen has dedicated her career to helping organizations effectively manage their payroll processes with Real Check Stubs.